Once again I get to discuss on whether investment depends on 'animal spirits', Schumpeterian entrepreneurialism or other confidence fairies. The evidence, as I noted here before, is quite overwhelming in favor of a simple and logical empirical regularity, namely: the accelerator. Below the last results from the Fair Model.

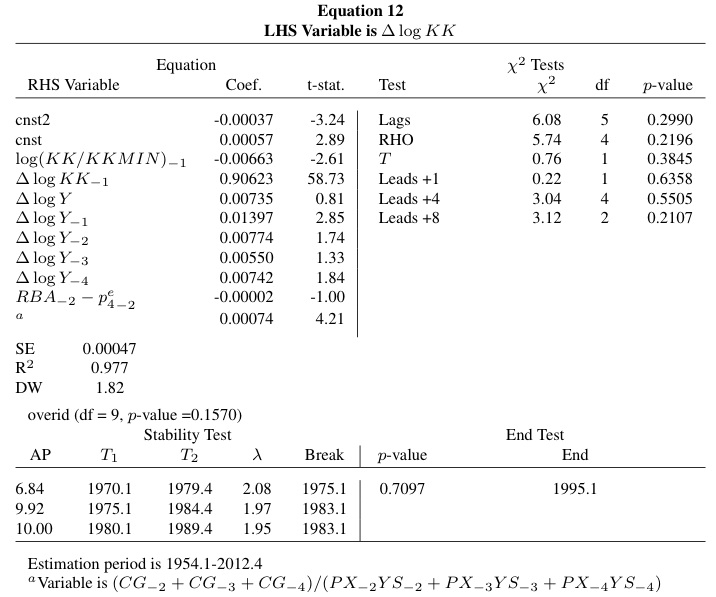

KK is the capital stock, RBA is the bond rate, and Y is income. Note that the coefficient on bond interests is insignificant, both statistically and in economic terms. What drives the change in the capital stock are the contemporaneous and lagged changes in the levels of income (demand). This is not only in the data, but is also quite logical. It says that firms increase their capital stock when demand increases (note that firms have always some spare capacity, so they are looking for permanent increases in demand). If there is no increasing demand there is no need to invest.

KK is the capital stock, RBA is the bond rate, and Y is income. Note that the coefficient on bond interests is insignificant, both statistically and in economic terms. What drives the change in the capital stock are the contemporaneous and lagged changes in the levels of income (demand). This is not only in the data, but is also quite logical. It says that firms increase their capital stock when demand increases (note that firms have always some spare capacity, so they are looking for permanent increases in demand). If there is no increasing demand there is no need to invest.

Not a surprising result, unless you for some other reason need the Superman theory of investment, in which the firm, the entrepreneur, the job creator is the hero that will save humanity from its mediocrity [have you been reading Ayn Rand again?].

PS: Ray Fair model uses the old Cowles Commission approach to macroeconometrics, which is much better than the new Dynamic Stochastic General Equilibrium (DSGE) models, that rely more heavily on calibration rather than estimation. He discusses the issue here.

Not a surprising result, unless you for some other reason need the Superman theory of investment, in which the firm, the entrepreneur, the job creator is the hero that will save humanity from its mediocrity [have you been reading Ayn Rand again?].

PS: Ray Fair model uses the old Cowles Commission approach to macroeconometrics, which is much better than the new Dynamic Stochastic General Equilibrium (DSGE) models, that rely more heavily on calibration rather than estimation. He discusses the issue here.

The accelerator explains investment until... it doesn't. It's a somewhat circular logic in that investment generates income and income generates investment. However, that which breaks the cycle is always left out -- and its arguably the most important "variable". Its usually an "event" of some form -- say, a financial crisis or something.

ReplyDeleteSo, the accelerator, like econometrics generally, is fantastic at explaining past data. But it doesn't help us anticipate future events very well at all. Nevertheless, its certainly a better starting point than some nonsense about confidence or Rational Expectations or whatever.

Not really. It's just derived demand. Again unless you believe in confidence fairies. It's one of Keynes mistakes that some posties keep alive. Again, logic and evidence.

DeleteAre you saying that the accelerator can explain breaks in investment? So, let's say that between 2002 and 2008 investment was driving more investment. But then something happened in 2008. That something was a financial crisis and the accelerator principle seems to me to have no ability to account for that.

DeleteIn Brazil employment has been very high but private investment low. To rule out confidence, or, clear rules is ludicrous

ReplyDeleteFirst of all the relation is about income and investment, not employment. Growth in Brazil has been low and private investment has followed an accelerator as is always the case. In Brazil part of the problem is the contraction of public investment, which is exogenous. Finally, employment is connected to growth through Okun's Law, and the fact that unemployment has been low with relatively low growth has more to do with a change in Okun's Law. Confidence is a catch all phrase for the size of ignorance. As Eccles says, it's obvious that with no growth there is no confidence, and once growth resumes there is confidence. You must believe in the Holy Ghost too.

DeleteBesides look at the evidence above, 97% of the changes in investment are explained by an accelerator equation.

Delete@Matías

ReplyDeleteI don't mean to be overly controversial here, but not even Keynes himself was altogether immune to the belief in the "Superman theory of investment" (btw, I find this a magnificently humorous way of expressing it, congrats)

It was Keynes, after all, who coined the "animal spirits" phrase: "spontaneous urge to action rather than inaction, and not as the outcome of a weighted average of quantitative benefits multiplied by quantitative probabilities" (General Theory, chapter 12, section vii)

In the same chapter Keynes explains at length how, in his view, confidence affected investment (and ultimately aggregate demand):

"The state of confidence, as they term it, is a matter to which practical men always pay the closest and most anxious attention. (...) There are not two separate factors affecting the rate of investment, namely, the schedule of the marginal efficiency of capital and the state of confidence. The state of confidence is relevant because it is one of the major factors determining the former, which is the same thing as the investment demand-schedule". (Chapter 12, section ii)

(...)

"This means, unfortunately, not only that slumps and depressions are exaggerated in degree, but that economic prosperity is excessively dependent on a political and social atmosphere which is congenial to the average business man. If the fear of a Labour Government or a New Deal depresses enterprise, this need not be the result either of a reasonable calculation or of a plot with political intent; - it is the mere consequence of upsetting the delicate balance of spontaneous optimism". (Chapter 12, section vii)

-------

And although Keynes admitted some of capitalism's failings ("its failure to provide for full employment and its arbitrary and inequitable distribution of wealth and incomes"), and foresaw the "euthanasia of the rentier", he argued for a legitimate and necessary role for capitalists.

In chapter 24, he distinguished from an unjustified return on investment (due to an alleged scarcity of capital) and a justified ROI ("This would not mean that the use of capital instruments would cost almost nothing, but only that the return from them would have to cover little more than their exhaustion by wastage and obsolescence together with some margin to cover **risk and the exercise of skill and judgment**").

From that to the Schumpeterian risk-taker (imagine Errol Flynn as Captain Blood or the Sea Hawk, but never as Robin Hood!), who goes around swashbuckling and making Ayn Rand sigh dreamingly, is just a step. :-)

Yep. Keynes got investment theory all wrong, as I noted above in my reply to Philip. Not just animal spirits, but worse the acceptance of the marginalist notion of the Marginal Efficiency of Capital that he says is quite similar to Fisher. I wrote on the topic here http://www.ppge.ufrgs.br/akb/encontros/2011/33.pdf

DeleteIf you totally get rid of the Keynesian notion of animal spirits you have to dump Minsky too. Minsky originally tried to tie his theory to the accelerator in a 1957 paper but found the attempt (rightly) to be unsatisfactory. So instead he fell back on the animal spirits theory essentially.

DeleteAgain, I'll say: the accelerator works great, until it doesn't. And yes, you can say that the fallout of a financial crisis leads to a deficiency of aggregate demand. It may or it may not. But you have to pinpoint the mechanism and you'll always come back to the animal spirits theory.

Not necessarily to animal spirits. Financing conditions and profitability can also be important. But I agree with you, saying that investment is all about the accelerator is as much a rejection of Keynes, Minsky and Marx as of the mainstream.

DeleteMinsky's views on investment are, much like his interpretation of the GT (note he says it's disequilibrium), problematic to say the least. But that does not mean that some of his important views on financial fragility have to be dismissed.

DeleteI agree that accelerator models of investment -- and more generally the strong links from current income to current expenditure -- should get more attention than they do. But let's be clear, if we really think the accelerator is *the* story of investment, we aren't just throwing out confidence theories and heroic Schumpeterian entrepreneurs. We're also throwing out Minsky (the financial instability hypothesis) and Marx (cyclical profit squeeze, etc.) Maybe that's what we have to do; maybe neither credit conditions nor profitability play any important role in aggregate investment fluctuations. But is that really what you think?

ReplyDeleteMost investment is financed out of retained profits. Credit conditions are important, but not determinant, since when the economy grows, and investment must adjust, credit is endogenously generated. Consumption is more likely to face liquidity constraints.

DeleteThe Marxist notion of cyclical profit squeeze (and Goodwin's 67 model, not his 51 non-linear accelerator) are profit-led and highly problematic.

The accelerator is not a theory--it is a reduced form relationship. The fact that lagged income enters with a positive coefficient says absolutely nothing about the importance of demand for investment. That is not an identified equation.

ReplyDelete"O"

Actually it is. Your discussing a particular method of measuring it. What the accelerator says is that there is a long run normal relation between productive capacity and demand, and that the former responds to the latter.

DeleteOk, I agree that the accelerator can explain long term patterns of investment. My question is: can it explain the kind of "heroic schumpeterian" guy who opens demand channels as he invests? I am thinking of people like josiah wedgwood.. does the accelerator falls back to a kind of "ex post" explanation where the only ones that are successful are the ones who can somehow sells his stuff?

ReplyDeleteOi Pedro:

DeleteSo Wedgwood (Darwin's grandfather!) could invest and expand capacity because there was an increasing demand (income) for china (pottery), associated to the expansion of demand in Britain. By the way, a process of import substitution. Yes he was entrepreneurial, but without demand expansion his heroic schumpeterian qualities would not necessarily help. The same goes for say John D. Rockefeller. His refinery would not have done well without a significant increase in the demand for lamp fuel, and more importantly the automobile boom. So, as Marx said, yes individuals matter, but in the context of an established situation.

Given the wealth of empirical evidence, it is hard to deny that investment is, in Matias' words, a "derived demand." But the ensuing discussion seems to interpret this as meaning that all investment is purely the result of income changes. We should note that (and I don't think Matias would disagree) there are components of investment that are autonomous. In other words, the Fair model that Matias posts above contains a constant. At certain historical moments there have indeed been large shifts in the autonomous component of investment, but let us not confuse the matter by claiming that investment as a whole is not a derived demand (which it clearly is).

ReplyDeleteYes, public investment is autonomous (see China), and residential investment is more responsive to interest rates (since it affects mortgages).

Deletenot even a mention that unemployment is the evidence that deficit spending is too low? no mention of demand leakages? that employment and investment is a function of sales/sales prospects?

ReplyDeletethat cycles can end when private sector credit expansion falters/govt. deficits get too low for financial conditions? that automatic fiscal stabilizers work?

easiest thing is to change the name to naked new Keynesianism

;)

Hi Warren:

DeleteIn all fairness none of those very reasonable things you suggest are affected or contradict the evidence above on the accelerator. The accelerator just says that investment is derived demand and that it is low as a result of the recession. And yes you need more fiscal expansion to get out of the crisis, which would also lead to an increase in investment (according to the accelerator). There is nothing New Keynesian about the accelerator, discovered by John Maurice Clark an institutionalist economist back in 1917.