The issue is back in the news. This time in Brazil (it was briefly an issue here when Trump did not reappoint Yellen, and then complained about Powell's interest rate where too high). At any rate, I always thought that there were good reasons for skepticism about central bank independence (CBI). As noted by Massimo Pivetti in this old piece on the Maastricht Accord and the, at that time, plan for the euro, the main reason to be doubtful is related to the interaction of monetary policy and fiscal policy. And as Quantitative Easing in the post-Global Financial Crisis has shown, central banks have become again fiscal agents of the state (never stopped being that, in all fairness).

The other important reason alluded by Pivetti for doubting CBI is the effects of the interest rate on the exchange rate and balance of payments. This is a quote from Pivetti:

And one could add, through the exchange rate, the effects on inflation also matter. This can be illustrated by the discussion of the Brazilian case. Lula has been very critical of the policies of the Brazilian Central Bank (BCB), and of the higher interest rates, since the campaign last year, and some sort of a truce has been in the works, with him being less direct (or at least that has been reported).

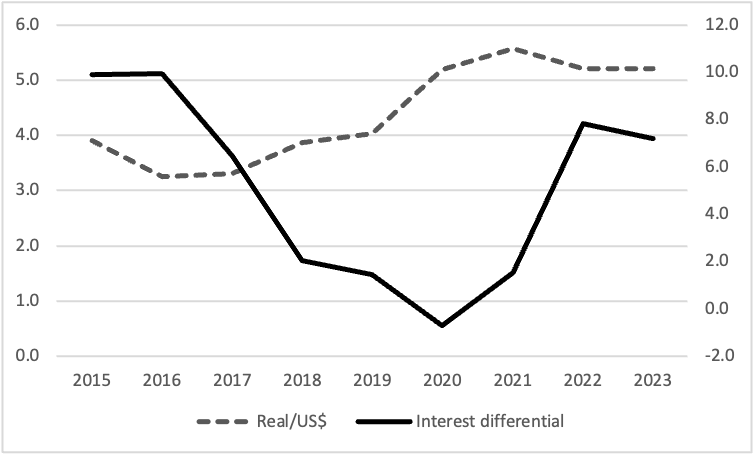

At any rate, the notion is that the higher interest rate is inimical to growth, even though Brazil did grow with relatively high interest rates in his first two mandates. The important thing to note is that Brazil had back then a relatively high and positive interest rate differential, that is a domestic nominal interest rates higher than the sum of external interest rate (the US rate) plus the risk premium (e.g. J.P. Morgan's Emerging Market Bond Index, EMBI), plus the expected nominal devaluation. In fact, as the interest rate differential (here just the difference of the BCB's Selic rate, the Fed Funds plus the EMBI) was coming down, the exchange rate depreciated.

Note that inflation accelerated and has been above the BCB's target only in more recent times, and the exchange rate is only one component of that. The higher prices of energy commodities, and the snags on the supply chain matter in the Brazilian case too. But the higher interest rate, and the higher and positive differential, did allow eventually for the stabilization of the exchange rate.

There is ample space to discuss how high the rate should be, but I'm doubtful that it can be close to zero or very low as suggested recently by André Lara Resende (that since my last post on his views, see here, has move away from Cochrane's fiscal theory of the price level, and closer to MMT; I just read his new book and that seems to be the case; on Cochrane's views on inflation see this video, also with John Taylor and Kevin Warsh).

Below the BCB's Selic rate and the Fed Funds for a longer period, starting after the stabilization of the Real Plan in the 1990s.

As one can see (Selic on the left, and Fed Funds on the right), the hike in the Brazilian rate has accompanied the hikes in the US, which are totally unnecessary, in my view, since inflation is cost push and not demand pull, but that's another

story. But the fact remains that the ability of central banks in the periphery to conduct monetary policy independently from what happens in the center is still curtailed. Note that the reduction of Brazilian rates, from higher levels (since a positive differential must be maintained to avoid capital flight and depreciation), was possible because the Fed Funds for the most part has been very low.

That's probably the more important discussion about the CBI. Not just independence from financial interests, as John Kenneth Galbraith used to suggest, but also the degree of independence in a world with a hegemonic currency.

PS: In the Brazilian case, the really important question for the Lula government will be his ability to increase spending beyond the fiscal ceiling. That, and the ability to eliminate hunger, and reduce poverty rates, would determine the political success of his administration.